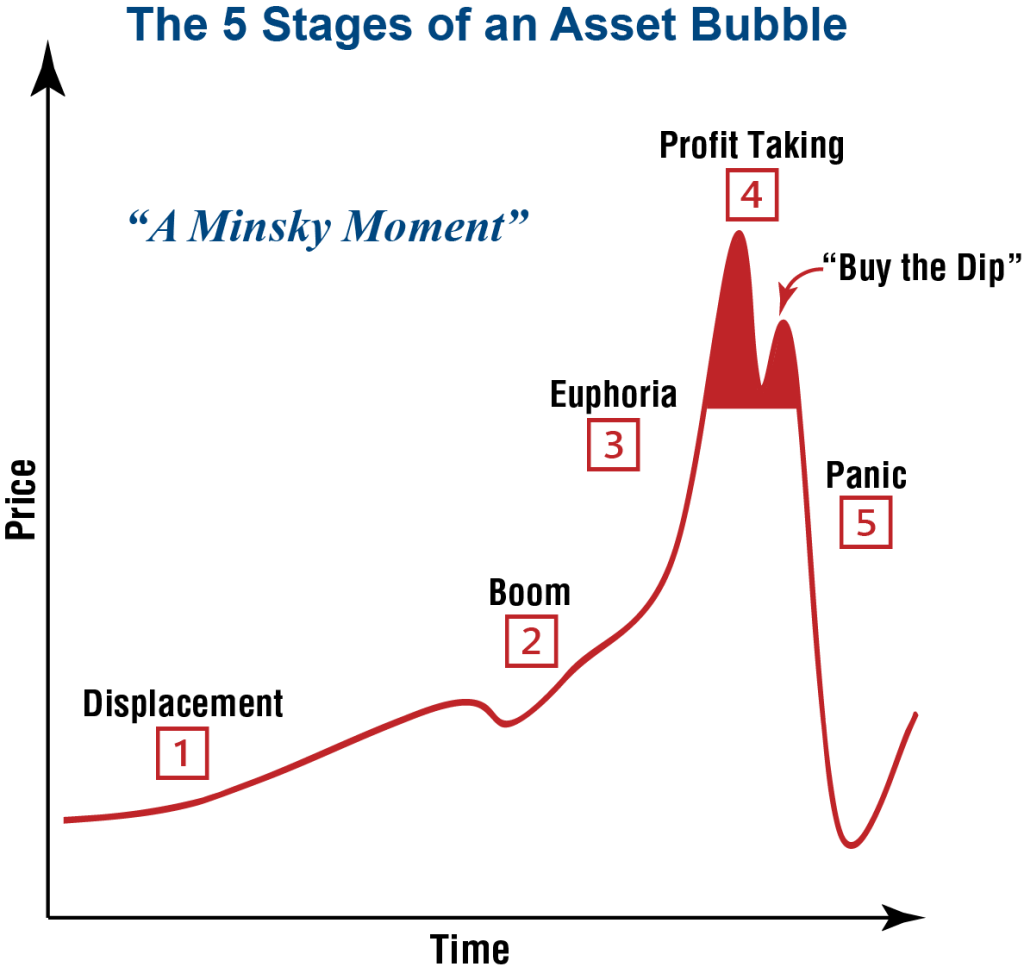

Stage  : Displacement

: Displacement

Displacement occurs when investors get enamored by a new innovation or technology. This first stage becomes a time for discovery as what was initially just an idea, quickly morphs into opportunity. Early adopters experience a genuine structural shift that significantly increases their expectations for profit.

Stage  : Boom

: Boom

As the new paradigm begins to prove itself, investment quickly accelerates. Profits start to rise and so do asset prices as more and more investors enter the market. Capital spending and debt begin to increase, but company balance sheets remain solid and optimism is high but rational.

Stage  : Euphoria

: Euphoria

During the Euphoria stage asset prices skyrocket as caution is abandoned, expectations for growth become unhinged, and speculators firmly believe growth will be indefinite. Leverage increases exponentially and private credit and off-balance sheet deals become the norm. This not only increases the use of debt, but also hides the true risk from the investing public.

Stage  : Profit Taking

: Profit Taking

At this stage, insiders and risk-managers quietly start selling positions and rotating into safer assets as the warning signs of an outright bubble become apparent. However, this is also one of the most difficult time periods to successfully navigate as speculation remains rampant and the “Buy-the-Dip” mentality can be tough to break. As John Maynard Keynes stated, “the markets can remain irrational longer than you can remain solvent.”

Stage  : Panic

: Panic

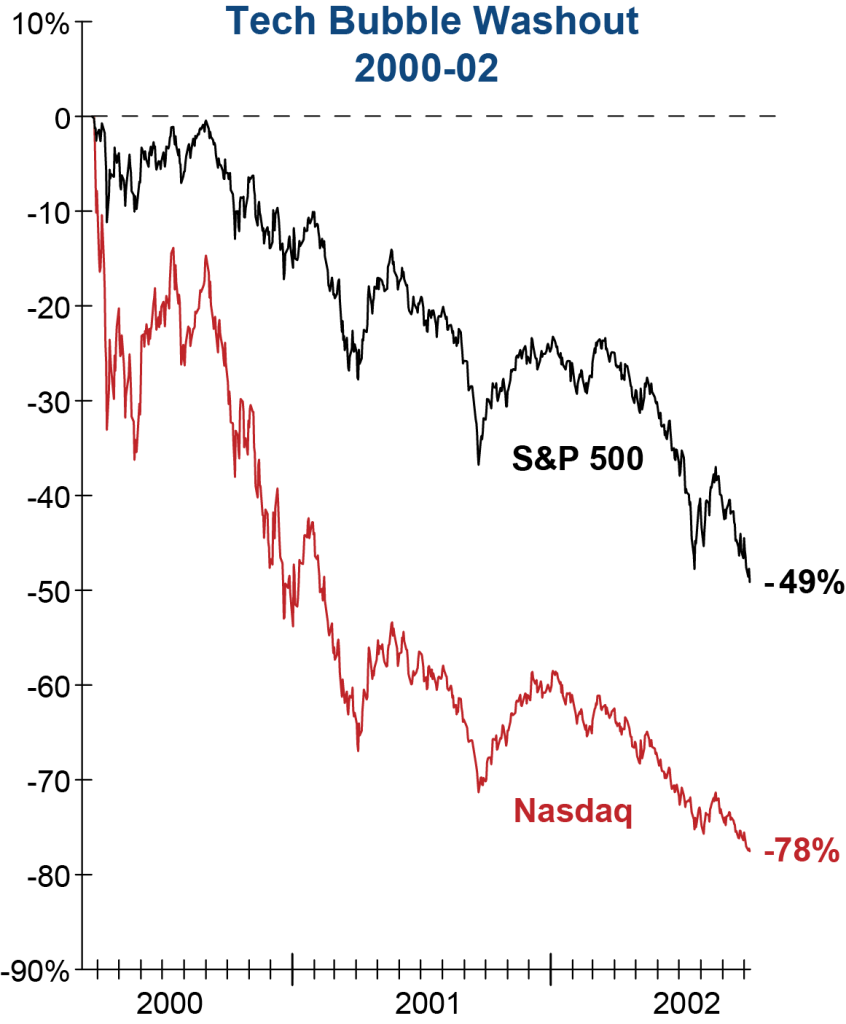

Asset prices fall as rapidly as they ascended during the Euphoria stage of the bubble. Liquidity evaporates and those who believed they could “time the exit” quickly find out how damaging a generational bear market can be. This is also when the risks of leverage and the interconnected nature of hidden debt asserts itself. As Warren Buffett once stated, “only when the tide goes out, do you discover who has been swimming naked.”

Only in the aftermath is an investment cycle formally labeled a “bubble.” While moving through Minsky’s five stages, participants are not acting irrationally. In their own minds, they are responding to rising prices, validating narratives, and seeing apparent proof that the opportunity is real. It is when the cycle breaks that the logic unravels, and the pattern and risk become obvious in hindsight.

Applying this model to today, we are concerned that the market has moved passed Euphoria and now resembles a dangerous environment when near-term Profit Taking can quickly turn into sheer Panic!